THE CHALLENGES AND OPPORTUNITIES OF OVERSUPPLY

• May 2025 •

Repeated large crop yields – significantly outpacing global demand

~

Tariffs, declining exports and low prices – difficulties for Madagascar

~

The vanilla market cycle – at the bottom, looking towards recovery

~

CNV opportunity – strategic stockpiles and price stability

As we enter the final stages of the 2023/24 Madagascar vanilla campaign, one thing has become abundantly clear: the world is awash in vanilla. While vanilla production is beginning to decline in some alternative origins such as Papua New Guinea and Indonesia, the world’s two largest producers—Madagascar and Uganda—continue to contribute significantly to global stockpiles.

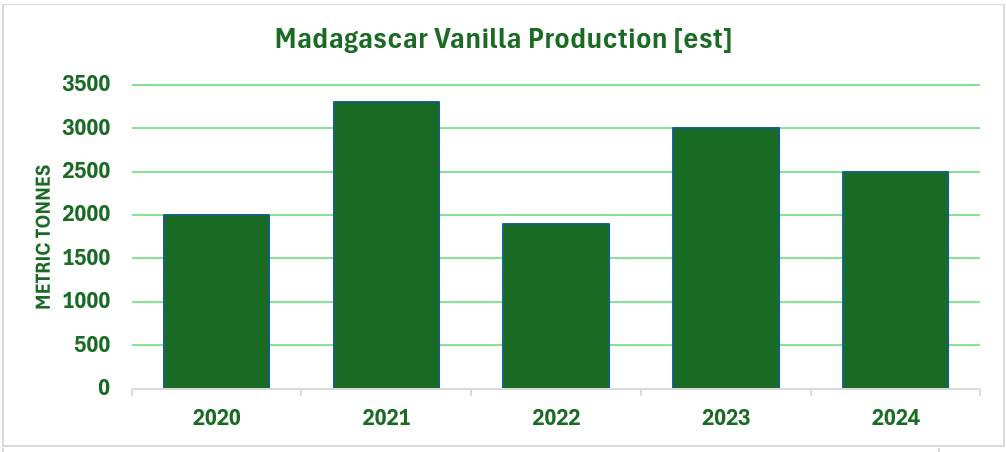

As anticipated, demand has cooled considerably compared to the previous campaign. This is largely due to extensive forward buying by major industrial users, which has not come close to reaching the levels seen in 2023/24. Madagascar is slowly recognizing that the over 4,000 metric tons exported in 2024 were primarily the result of strategic stockpiling rather than a surge in demand. Current estimates suggest that only around 1,500 metric tons have been exported from Madagascar so far from the 2024/25 crop—well below expectations.

Adding to Madagascar’s challenges, U.S. tariffs have recently emerged as a new obstacle. A few months ago, and for reasons that remain unclear, a 47% tariff was imposed on all Malagasy goods entering the U.S. market, including vanilla. This move is particularly perplexing given that Madagascar primarily exports high-value agricultural commodities such as vanilla, coffee, and cacao to the U.S., while importing virtually nothing in return. The resulting trade imbalance is not something that tariffs can realistically correct. Madagascar is one of the poorest countries in the world, and there is little the U.S. can export that Malagasy buyers can afford. Although the tariff has since been reduced to a base rate of 10%—now also applicable to Uganda and other vanilla-producing nations—it remains difficult to justify taxing agricultural products from countries that cannot grow vanilla commercially and have limited economic means.

Tariffs aside, the largest issue facing Madagascar and the global vanilla market is oversupply. We estimate that Madagascar’s 2025 crop could easily exceed 3,000 metric tons. In addition, there is likely a substantial volume of unsold 2024 vanilla and carryover material from prior years. When accounting for unsold vanilla from other origins, the global supply available in 2025 could exceed 6,000 metric tons—equivalent to roughly two and a half years of global demand, which is currently estimated at 2,500–3,000 metric tons annually.

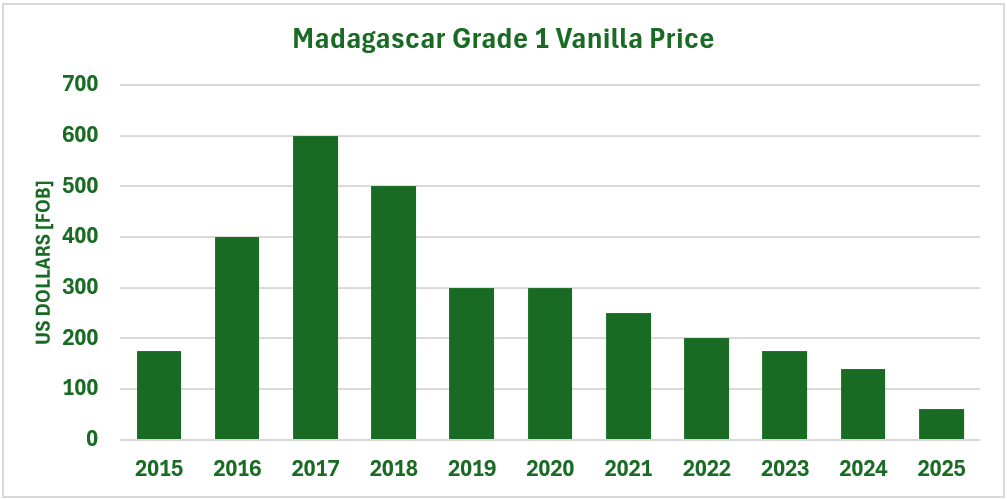

Export prices from Madagascar are quickly approaching historical lows, and indicative prices for 2025 green vanilla suggest they may drop even further—despite the $4.00/kg export tax, which we expect to remain in place despite U.S. pressure to eliminate it.

For several months, rumors have circulated about potential government measures to stabilize the vanilla market. Proposals have included a drastic reduction in the number of exporters, an increase in the minimum export price, an increase in the export tax, and the establishment of a minimum farmgate price for green vanilla. In our view, the only measure with clear enforceability is the CNV export tax, as exporters must pay this levy before shipping their goods. This tax, if strategically managed, could serve as a tool to mitigate the damage caused by the global vanilla glut.

The CNV tax has already raised tens of millions of dollars, reportedly earmarked to support the vanilla industry. We’ve heard of possible investments in infrastructure, such as a vanilla testing laboratory in the Sava region and a vanilla-themed museum and store in the capital, Antananarivo. While these are worthwhile projects, given the urgency of the current crisis, we believe a more immediate and impactful use of the funds would be direct investment in vanilla itself.

Several foreign companies have profited over the years by speculating on vanilla. One of today’s largest vanilla traders, based in the Netherlands, began as a speculator after the 2003/04 crisis. Like all commodities, vanilla follows a boom-and-bust cycle. The last peak-to-peak cycle ran from 2003 to 2016—approximately 13 years. We are now nine years into the current cycle. While we cannot predict the exact timing of the next price rebound, history strongly suggests that a recovery is inevitable.

So, why shouldn’t the Malagasy government leverage CNV revenues to purchase vanilla locally and build a government-controlled strategic reserve? Based on current CNV revenues and prevailing vanilla prices, the government could accumulate over 1,000 metric tons. Additional funding for warehousing and maintenance could be drawn from existing and future CNV collections. Since the CNV tax is paid by foreign buyers, this initiative would carry minimal financial risk for the government.

Such a program would not only stabilize the market but also demonstrate responsible use of CNV funds—potentially quelling persistent rumors of misappropriation. Industrial-grade vanilla, which accounts for over 80% of global demand, would be the logical target for this initiative, provided the product is properly cured and dried for long-term storage. This approach would require discipline, expert management, and patience—but with no local taxes on internal purchases, the government’s base cost would be significantly lower than export prices.

In 2016/17, vanilla prices soared to USD $600/kg for Grade 1 and over $400/kg for Grade 3. While we do not predict a return to those levels, we do believe that the government could ultimately profit significantly while helping to stabilize one of its most valuable export commodities. This bold action would benefit all stakeholders in the vanilla value chain.

Absent any concrete action, we fear vanilla prices will fall even further later this year.

Uganda has largely followed Madagascar’s pricing trends. However, prices in Indonesia and Papua New Guinea appear to have already bottomed out at higher levels.

As a result, production is beginning to decline in those regions, which cannot afford to match Madagascar’s pricing and rely instead on the unique flavor profiles of their vanilla to maintain market presence. We do not expect more than a combined 300 metric tons of cured vanilla from Indonesia and Papua New Guinea in 2025.

Meanwhile, Madagascar and Uganda are expected to produce robust crops again in 2025—approximately 3,000 metric tons from Madagascar and 300–400 metric tons from Uganda. In Madagascar, the 2025 green vanilla campaign has already begun in the north, with prices as low as $1.50/kg (approximately 7,000 Ariary). If this trend continues and there is no government intervention, export prices for the 2025 crop—especially for Grade 1 extraction and gourmet vanilla—are likely to fall further. Uganda is expected to continue mirroring Madagascar’s price trajectory, providing some level of competition in the global market. Although volumes from Indonesia and Papua New Guinea will diminish, their products will retain market relevance due to their distinctive flavor profiles.

We believe the global vanilla market is now entering the final phase of a prolonged period of oversupply and declining prices—a phase that could persist for several more years. Quality will remain generally good, though not exceptional, as preparers and exporters cut costs to preserve ever-thinning margins. The market will stay intensely competitive, with a vast number of vendors vying for a limited pool of buyers. Unfortunately, as is often the case, the vanilla-dependent farming communities of Madagascar will bear the brunt of the downturn.

We strongly encourage vanilla buyers to consider securing the longest possible coverage their suppliers can offer. Given the historical price volatility of vanilla, the short-term downside risk is greatly outweighed by the long-term potential for price recovery.

Aust & Hachmann (Canada) Ltd

The market reports that we issue are based strictly on our opinions and observations. We believe we have presented a reasonably accurate portrayal of the global vanilla market in very general terms. The reports date back almost 20 years and are all available on our web site:

https://www.austhachcanada.com/reports/

Recent Comments